Ai

Why these 8 Industries and 50 Caribbean Companies are One Startup and One Ai Tool Away From Disruption.

THE

INCUMBENTS

ARE EXPOSED.

This article was inspired by this Instagram post. They, Explaining the Caribbean, published a list of the highest-grossing Caribbean Companies.

On the post, it said “The Caribbean is home to dozens of major companies generating hundreds of millions, and even billions, in annual revenue.

These are the 50 highest-grossing companies in the Caribbean based on their 2025 revenue

Coming in the number 1 spot, having generated $US2.32B in 2025, is the National Commercial Bank Financial Group Limited of Jamaica, while West Indian Tobacco Company Limited of Trinidad & Tobago rounds out the top 50, with US$28.3M in revenue

Jamaica dominates with 20 companies in the Top 50, with Trinidad & Tobago claiming 15 spots. That is 70% of the Top 50 belonging to both nations 🇯🇲🇹🇹

All figures are in USD and represent revenue reported for the 2025 financial year (or the closest available 2025 reporting period where applicable).”

This is a great way to get a beautiful snapshot of companies, their industries, and reported revenue.

CLAUDE & I

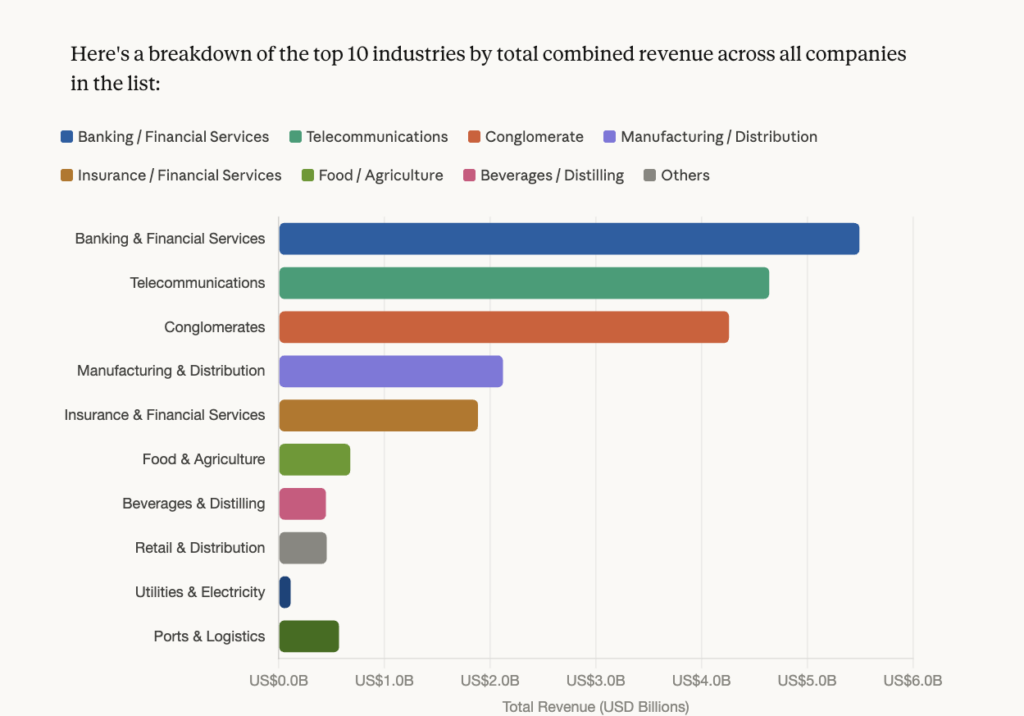

I asked Claude Ai to analyse these numbers and create a list of the top 10 industries making these companies a lot of money. It produced this:

ere’s the ranking with key takeaways:

1. Banking & Financial Services — ~US$5.5B — The dominant sector, anchored by NCB Financial Group (US$2.32B), Republic Financial Holdings (US$1.14B), and several regional banks across Jamaica, T&T, Guyana, and Barbados.

2. Telecommunications — ~US$4.64B — Driven almost entirely by Liberty Latin America and Digicel, the three entities together account for the bulk of this.

3. Conglomerates — ~US$4.26B — Massy Holdings, ANSA McAL, and Goddard Enterprises span multiple sectors under one umbrella.

4. Manufacturing & Distribution — ~US$2.22B — A broad category including Seprod, Wisynco, PBS, Derrimon, and Banks DIH.

5. Insurance & Financial Services — ~US$1.88B — Led by Guardian Holdings (US$1.07B) and Sagicor Group Jamaica (US$814M).

6. Food & Agriculture — ~US$676M — Jamaica Broilers and LASCO Manufacturing.

7. Beverages & Distilling — ~US$446M — Banks DIH, Demerara Distillers, and Angostura Holdings.

8. Retail & Distribution — ~US$453M — S.L. Horsford, PBS, and similar companies.

9. Utilities & Electricity — ~US$112M — Grenlec (Grenada) and LUCELEC (St. Lucia).

10. Ports & Logistics — ~US$569M — PLIPDECO, Kingston Wharves, and TransJamaican Highway.

The clear takeaway: Finance and Telecoms dominate the Caribbean corporate landscape, with Jamaica and Trinidad & Tobago producing the most companies on this list.

Then I asked Claude Ai this question:

How can tech, Ai, Fintech, digital platforms, globally scalable companies disrupt all of this and help create a modern Caribbean economy?

This is one of the most important economic questions the Caribbean can ask right now, I believe. The timing is genuinely ideal- the Region has real structural advantages that tech can amplify, and we are now firmly in the AI Age, which gives advantages to those who can leverage those AI tools and platforms, those who have pattern recognition, dot connecting, and take action now skills.

Anyway, what follows is an article written by me (90%) and Claude AI.

How AI, fintech, and digital platforms will disrupt the region’s biggest industries and who should build them.

Eight industries. Billions in combined revenue. Decades of geographic protection. And which one of them is ready for what’s coming? This is a sector-by-sector breakdown of where tech, AI, and digital platforms will crack the Caribbean economy wide open and what can be built in the space left behind.

The

comfortable

era is over.

The Caribbean’s largest companies built their dominance the old-fashioned way: they showed up, they stayed, and they waited for competitors who never came. Islands create natural monopolies. Distance is a moat. Regulatory capture is a strategy.

That era is ending. Digital platforms don’t respect coastlines. A fintech built in Miami or Lagos can acquire a Jamaican customer before a local bank can open an account. A streaming platform in Los Angeles can monetise Caribbean culture before a Caribbean creator sees a cent. A global OTA can sell a Barbados hotel room at a higher margin than the hotel itself earns.

The question is not whether disruption comes to the Caribbean. It is whether Caribbean entrepreneurs are the ones who deliver it or whether they watch it happen from the outside again.

The breakdown:

8 SECTORS.

8 VERDICTS.

Every major industry in this Caribbean list was assessed for vulnerability, opportunity, and what a digital challenger could and probably should build.

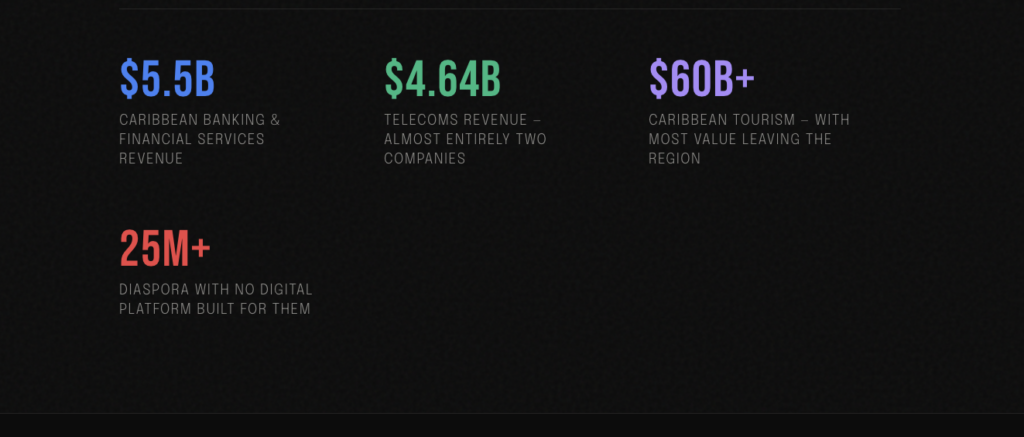

Banking & Fintech

~US$5.5B combined revenue

Incumbents at risk: NCB Financial Group · Republic Financial Holdings · CIBC Caribbean · Scotiabank T&T · First Citizens

Banks that charge 7–9% to move money between islands. Banks that still require a branch visit to open an account. Banks that have never had to compete.

Disrupt

Caribbean remittance fintech – Blockchain or Stablecoin rails cutting fees from 8% to under 1%. The $7B flowing home annually is being taxed by Western money transfer operators. That ends with a regional challenger.

Disrupt

Mobile-first neobank for the unbanked across smaller islands – Grenada, St. Lucia, Belize. No branch, no minimum balance, no paper forms. Account opened in 3 minutes on a phone.

Build

AI credit scoring using alternative data – mobile spend, utility payments, merchant history. Extends credit to the SMEs that Caribbean banks systematically ignore. The loan book that never existed.

Build

Unified Caribbean payment rail – a regional infrastructure layer replacing fragmented SWIFT dependencies. One integration for merchants to accept payments across all 15 CARICOM jurisdictions.

Enable

RegTech for multi-jurisdiction compliance – automate AML/KYC reporting across CARICOM simultaneously. The compliance burden is the reason most fintechs avoid the region. Remove it.

Scale potential

Global. Total Diaspora remittance flows across all Caribbean countries were projected to hit approximately US$20.9 billion in 2025. A 1% fee reduction returns hundreds of millions annually to families. The neobank market spans 44 million people across the Caribbean basin -before the diaspora market is even counted.

TELECOMS

~US$4.64B combined revenue

incumbents at risk

Digicel Group · Liberty Latin America · Liberty Caribbean · Liberty Puerto Rico

“Some of the most expensive mobile data in the world. A digital divide that splits larger islands from smaller ones. Two companies that, between them, have never really had to fight for a customer.”

Disrupt

Satellite internet cooperative – pool demand across small islands to negotiate wholesale pricing with Starlink and competitors. Break the cable duopoly that has held the region hostage for two decades.

Build

Caribbean sovereign cloud infrastructure – regional data centres in-territory, reducing dependence on US and EU cloud providers. Data sovereignty plus latency advantages for regional businesses.

Build

EdTech platform on improved connectivity rails – Caribbean curriculum delivered digitally across all CARICOM nations. Cheaper data makes education the first killer application.

Enable

IoT platform for the physical economy – smart grid monitoring, crop sensors, port logistics tracking. The telecoms infrastructure that exists today is dramatically underutilised by the industries that need it most.

Scale potential

Foundational. Cheaper data doesn’t just disrupt telecoms -it unlocks every other digital sector simultaneously. This is the infrastructure bet. Whoever builds the next connectivity layer owns the on-ramp to the entire Caribbean digital economy.

CONGLOMERATES

~US$4.26B combined revenue

Incumbents at risk

Massy Holdings · ANSA McAL · Goddard Enterprises · Pan Jamaica Group

“Sprawling empires built on physical distribution, brick-and-mortar retail, and import relationships. Powerful in 1995. Structurally fragile in 2025. No digital consumer layer. No data strategy. No defence against a focused challenger.”

Disrupt

Caribbean e-commerce marketplace – aggregate regional merchants, solve last-mile island logistics, and own the consumer relationship that conglomerates have never bothered to build digitally. The “Caribbean Amazon” is still unclaimed.

Enable

AI supply chain optimisation – reduce food waste and stockouts across island retail, where import logistics are expensive and unpredictable. The savings on a well-optimised island supply chain are enormous relative to operating costs.

Build

B2B SaaS for Caribbean SMEs – inventory management, procurement, and accounting tailored to multi-island operations. Every business that the conglomerates service is a potential direct software customer.

Build

Digital loyalty and consumer data platform – the conglomerates touch millions of consumers daily and collect almost no actionable data. The company that builds this layer doesn’t need to own a single warehouse.

Scale potential

Regional first, then Latin America. The playbook proven in the Caribbean – multi-island, multi-currency, multi-jurisdiction e-commerce – scales directly to 650 million Spanish and English speakers in the Americas. The Caribbean is the testing ground for a much larger opportunity.

FOOD & AGRICULTURE

~US$676M combined revenue

Incumbents at risk

Jamaica Broilers Group · LASCO Manufacturing · Wisynco Group · National Flour Mills

“A region that imports 60–80% of its food. No precision agriculture. Climate catastrophe on one side, food insecurity on the other. And a globally beloved food culture that earns almost nothing for the people who created it.”

Build

AgriTech platform for the tropics – soil sensors, satellite imagery, and AI crop advisory designed specifically for Caribbean conditions. The tools exist. None of them has been trained on Caribbean soil, Caribbean rainfall patterns, or Caribbean crops.

Build

Vertical farming for island markets – controlled environment agriculture that reduces import dependency and builds genuine food security. Climate-resilient, land-efficient, and applicable across every island regardless of terrain.

Enable

Blockchain provenance for premium exports – verified origin for Caribbean rum, coffee, cacao, and spices. Premium pricing through authenticated provenance. The Champagne model applied to the region’s most distinctive products.

Disrupt

Direct-to-diaspora food e-commerce – Caribbean food brands shipping globally to 25M+ diaspora members. The demand is enormous. The supply chain barely exists. The brand story writes itself.

Scale potential

Global export play. Caribbean food has a premium global brand. Verified origin plus direct-to-consumer distribution equals massive margin uplift. The diaspora food market alone — before broader consumer interest — is worth hundreds of millions annually.

TOURISM

$60B+ industry – largely undigitised

The problem

Foreign OTAs · International hotel chains · Foreign airlines · Fragmented local operators

“Tourism is the Caribbean’s largest industry and the Caribbean captures the smallest share of its own value. Booking.com, Expedia, and Airbnb take the margin. Marriott and Hilton take the brand. The region provides the sunshine and the labour.”

Build

Caribbean-owned OTA and experience platform keeps the booking margin in the region. Currently, ~$2B+ flows annually to foreign platforms. A Caribbean-first travel platform built for Caribbean properties, Caribbean tours, and Caribbean experiences.

Build

Digital nomad relocation infrastructure – visa processing, co-working, housing, and community for the 35M+ remote workers seeking warm-climate bases. Caribbean governments need to have more Digital Nomad visa programmes, and someone needs to build the platform around them.

Enable

AI personalisation for Caribbean tourism drives spend-per-visitor from experiences, not just bed nights. The revenue-per-tourist in the Caribbean is structurally low because the discovery and booking of local experiences is completely broken.

Disrupt

Tokenised fractional property ownership -Caribbean real estate sold to diaspora globally via digital assets. Fractional stakes in villas, boutique hotels, and development projects. Turns the diaspora’s aspiration to own Caribbean land into a liquid, accessible product.

Scale potential

Enormous. Tourism is a $60B Caribbean industry. Capturing even 10% of the current value leakage money that flows to foreign OTAs, hotel brands, and airlines would represent $6B+ annually staying in the region. This is the single largest recapture opportunity in the Caribbean economy.

ENERGY & CLIMATE

$4B+/year in fossil fuel imports

Incumbents at risk

Grenada Electricity Services (Grenlec) · St. Lucia Electricity Services (LUCELEC) · PLIPDECO · all legacy utility monopolies

“The highest electricity prices in the world average $0.30 per kWh. Near-total dependence on imported fossil fuels. A climate crisis that threatens to destroy the region’s two largest industries: tourism and agriculture. And utility monopolies that have every incentive to keep things exactly as they are.”

Build

Solar-as-a-service platform, zero-down solar for Caribbean homes and businesses on a subscription model. The Caribbean has more solar irradiance than almost anywhere on Earth. Its households pay some of the highest electricity prices. This is not a complicated equation.

Build

Caribbean carbon credit marketplace, Caribbean forests and marine ecosystems as verified carbon sinks sold to global corporates. The region’s natural capital is worth billions. Almost none of it has been monetised for the communities that protect it.

Disrupt

Community microgrids and peer-to-peer energy trading bypass legacy utility monopolies entirely. Enable communities to generate, store, and trade their own power. The technology exists. Caribbean regulatory environments are slowly opening. First movers take everything.

Enable

Parametric climate insurance predictive storm damage modelling, and automatic payouts for Caribbean households and businesses. Current insurance penetration is under 20%. A digital-first, parametric model changes the risk economics entirely.

Scale potential

Transformational. The Caribbean spends ~$4B/year on imported fossil fuels. A successful solar transition doesn’t just reduce costs, it redirects that capital from foreign oil markets into Caribbean households and businesses permanently. It is the single most important economic lever the region can pull.

HEALTH & MEDTECH

Largely informal, undercounted & underserved

Incumbents at risk

NCB Insurance · Sagicor Group (insurance arm) · fragmented public health systems

“Diabetes and hypertension rates are among the highest in the world per capita. Specialist medical care concentrated in a handful of places. Caribbean residents flying to Miami or London for treatment. A health insurance market built on actuarial models from the 1980s?”

Build

Pan-Caribbean telemedicine network specialist access without flying to Miami or London. Connect every Caribbean island to a shared pool of specialist physicians. The model that works in rural America and sub-Saharan Africa works here too.

Build

AI chronic disease management via WhatsApp – diabetes and hypertension coaching for high-prevalence populations, delivered through the platform they already use every day. The highest-impact health intervention the Caribbean can make at the lowest possible cost.

Enable

Caribbean health data cooperative anonymised population health data, built with a robust consent framework, monetised for pharmaceutical research. The Caribbean’s unique genetic diversity and disease profile is a research asset worth hundreds of millions. Currently uncaptured.

Disrupt

Digital-first health insurance dynamic pricing based on lifestyle and biometric data, replacing legacy actuarial models. The incumbents are pricing risk using decades-old data. A challenger with real-time data wins on both price and profitability.

Scale potential

Regional plus export. The telemedicine and chronic disease management opportunity is regional. The health data cooperative and the insurance disruption have global venture scale. Jamaica already attracts medical tourists a digital platform built around that reputation multiplies it tenfold.

CREATIVE ECONOMY

$1B+ in music alone — almost all offshore

The structural problem

Foreign record labels · Global streaming platforms · International fashion conglomerates · Western media companies

“The Caribbean’s most powerful global export – its culture generates billions of dollars worldwide. Caribbean creators see almost none of it. Reggae, Soca, Dancehall, and Kompa. The aesthetics, the rhythms, the language. Extracted, commercialised, and monetised by institutions that have no stake in the region’s future.”

Build

Caribbean creator monetisation platform -direct fan funding, streaming royalties, merchandise, and live event ticketing, built around Caribbean artists and their global audiences. The infrastructure of Spotify and Patreon wasn’t built to provide for a Caribbean creator in any meaningful way.

Build

Caribbean IP licensing and royalty management platform – the music rights currently exploited by foreign labels, recaptured digitally. A Caribbean-owned rights management company that negotiates, tracks, and distributes royalties for the region’s artists at scale.

Enable

AI creative tools trained on Caribbean culture -music production, visual art, and film tools that understand Caribbean aesthetics, not approximate them. Built with Caribbean artists. Compensating Caribbean artists. Owning the Caribbean creative stack before Silicon Valley decides to build a “tropical” filter.

Disrupt

Global Caribbean cultural subscription – a platform for the 25M diaspora to access Caribbean content, food, fashion, and community globally. The cultural connection that the diaspora craves and that no platform – not Spotify, not Netflix, not Instagram – has been built to serve.

Scale potential

Global recapture. Caribbean music alone is a $1B+ global industry with most value captured offshore. The creative economy is the sector where the gap between value created and value retained by Caribbean people is most obscene – and therefore where the opportunity for digital recapture is most dramatic.

The Caribbean has never lacked culture, talent, or the raw ingredients of a great economy. What it has lacked is the infrastructure to own what it creates. That infrastructure is now buildable. The only question is who builds it.

THE WINDOW

IS OPEN.

The companies at the top of the Caribbean revenue rankings are not invincible. They are geographically protected, and geography is the one moat that the internet has always dissolved. The bank that charges you 8% to send money to your mother. The cable company has not had a meaningful competitor in twenty years. The conglomerate that distributes goods across six islands without a single digital product to show for it. These are not businesses built on exceptional excellence. They are businesses built on the absence of alternatives and yep, some lobbying too.

The alternatives are now possible to build. Not cheap, not easy, not without risk – but possible, in ways they have never been before. The cost of building a software company has collapsed. The diaspora is a pre-existing global customer base for everything Caribbean. AI tools have lowered the barrier to building products that would have required teams ten times the size a decade ago.

The honest challenge is capital, talent density, and regulatory will. Caribbean venture capital remains thin. But the Venture Studio model is rising. The governments that should be creating the conditions for digital challengers are often the ones protecting the incumbents. The talent that leaves for London, Toronto, and New York and rarely comes back takes institutional knowledge with it every time.

But these are problems that have been solved in smaller markets, with fewer natural advantages, and with less cultural momentum than the Caribbean carries. Estonia built a digital economy with 1.3 million people. Korea turned cultural exports into a $12 billion global industry. Nigeria’s tech sector crossed $1 billion in funding in a single year. None of them had what the Caribbean has: a globally beloved culture, a 25-million-strong diaspora with capital and appetite to invest, and a climate that the rest of the world would pay almost anything to live in.

The incumbents are exposed. The window is open. What gets built next is the question that matters.

And as I wrote and edited this, I wrote a short list of companies in Global Caribbean I know that are and have built things to challenge the status quo…I will reveal who they are soon, and they, too, will reveal themselves.

These are fricking amazing times!!

-

Trends16 years ago

376,580 Trinidadians now on Facebook, 40% of their population Online.

-

Trends16 years ago

Jamaicans pour unto Facebook 429,160 now on the social network

-

Trends16 years ago

JamaicaObserver.com steps it up again with Social Media Plugins

-

eCommerce3 years ago

eCommerce3 years agoHow Amazon.com Shipped Directly To My door in Jamaica, Finally!